The Ctrack Transport and Freight Index records marginal increases

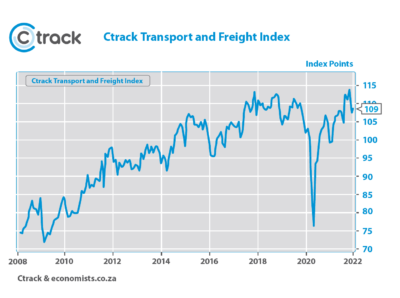

The Ctrack Africa Transport and Freight Index (CTFI) reached a record high in November 2021 but moderated somewhat in December and increased just marginally in January 2022. The CTFI advanced by just more than one point in January 2022 to an index level of 109 compared to 107.6 in December.

This incremental increase still reflects ongoing global supply chain problems, while the sub-sectors that make up the Ctrack Transport and Freight Index reflected a mixed bag in terms of performance. Three of the six sectors moderated, namely, Sea Freight, Air Freight, and Storage. Countering the weakness evident in these sub-sections, the star performer Road Freight continued to power ahead in January, while Rail Freight showed an unexpected monthly increase, and transport via pipeline has also recovered notably, wiping out the moderation that was evident in the past three months.

On a quarter-on-quarter basis and on a three-month moving average basis, the CTFI is tracking 0.7% higher in the three months to January 2022, compared to the three months ending October 2021, while a monthly increase of 1.3% was recorded in January 2022. On an annual basis, the CTFI is tracking 6.4% higher in January than a year earlier. Although it is still early days, it could signal some acceleration in economic activity levels early in the first quarter of 2022.

“Continued growth in the Ctrack Transport and Freight Index is great to see given the variety of external factors, ranging from supply chain issues to rising fuel prices, contributing to the difficulty in doing business in the transport sector,” said Hein Jordt, Chief Executive Officer of Ctrack Africa.

Graph 1 The Ctrack Transport and Freight Index monthly

Taking a closer look at the different sub-sectors revealed that Road Freight continued to power ahead. Road Freight transport, which contributes 47.8% to the CTFI, increased by 14.6% compared to January 2021, based on a three-month moving average. Quarterly, Road Freight improved by 1.2% in the three months ending January 2022, compared to the three months ending October 2021, while a monthly increase of 2.0% was recorded in January 2022.

Road Freight continues to benefit from the troubles experienced by Transnet Freight Rail (TFR). Transnet Freight Rail recently indicated that they hope to entice trucking companies operating between Gauteng and Durban and on other routes to consider coming in as private rail operators as the company admits it is facing major challenges. Still, only time will tell if trucking companies would be interested in taking on that additional business risk.

The strong performance of Road Freight is hopefully also a sign of economic recovery, as we do forecast that the South African economy will continue to recover gradually in 2022, from the significant contraction recorded in 2020. With the low base effects a thing of the past, growth in 2022 will better reflect the underlying momentum in the South African economy. The only mediocre real growth of about 2% is forecast for the three years to 2024, with several notable risks and ongoing hampering factors still keeping a lid on growth, including intermittent load shedding, higher inflation, and interest rates, and slow progress on much-needed structural reform.

“While the growth in Road Freight continues to impress, profit margins could face additional pressure in the light of ongoing substantial fuel price hikes. This makes the efficient running of fleets imperative for operators who want to remain profitable,” added Jordt.

Another factor that will continue to play a role in near-term comparisons is the fact that November 2021 was a very strong month, with the Road Freight index beating its previous high by 18.7%. September and October 2021 also recorded highs; thus, subsequent months compare to these high activity months.

Rail freight surprised to the upside in January 2022, but the bigger picture remains under a cloud.

Despite a surprising strong monthly increase of 10.3% in Rail Freight in January 2022 (weighting of 22.6% in CTFI), one month does not make a trend. The volume of goods transported by Rail Freight is still 1.4% below year-ago levels, and if a three-month moving average of the volume of freight transported via rail is considered, Rail Freight is still 7.9% below year-ago levels.

Rail Freight’s problems are deep-rooted, structural, and unlikely to be fixed in the short to medium term. The utility is struggling to operate on the Gauteng-Durban corridor, an important route for automotive exports and imports. Due to temporary speed restrictions caused by poor infrastructure – a result of underinvestment – cable theft and community encroachment on the network are just some of the issues they face. This has resulted in massive delays, for example, doubling the time it should take to travel between the container terminal in City Deep, Johannesburg, and Durban’s port.

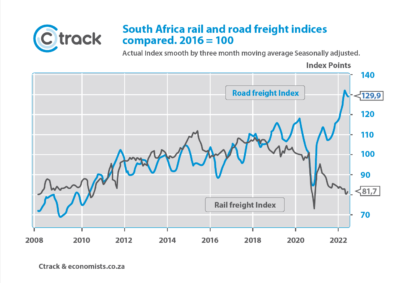

The change in fortunes between rail and road is depicted in the graph below, which illustrates how goods have moved to road, particularly since the COVID-19 lockdown. According to Business Times, Transnet indicated that the rail network is under attack from highly organised cable theft syndicates, with 395km of cable stolen in 2019/2020, 700km in 2020/2021, and more than 1 000km thus far in the financial year ending 2022. Furthermore, in the financial year ending 2021, the rail entity spent R1.6bn on security and R400m on replacing lost cables.

Graph 2: The Rail and Road Freight indices compared.

Transport via pipeline (with a weighting of 2.2% in CTFI) increased notably during January 2022, with a 7.2% increase. However, the three-month average reveals that volumes transported via Pipelines are still 15.9% below the levels experienced a year ago.

The other three sectors, with a combined weighting of almost 28% in the CTFI, contracted on a monthly basis in January 2022. Sea Freight, Air Freight, and storage declined by 11.0%, 5.8%, and 3.4% respectively in January, compared to December 2021. These sub-sections do attract a fair amount of volatility on a month-to-month basis, thus considering a three-month moving average and comparing to a year earlier, revealed that all three sectors are still in positive territory. Air Freight increased by 9.5% on a year ago, second just to Road Freight’s growth of 14.6%. Sea Freight treaded water with growth of only 0.3% on a year earlier. Storage and warehousing increased by 1.2%, although this sector showed a lot of volatility, as global supply chain developments remain a concern as the trend of stockpiling goods in fear of future shortages continues.

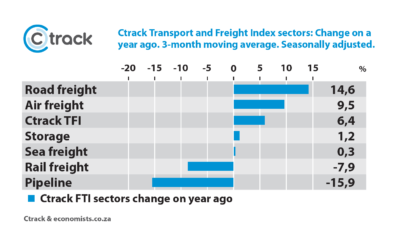

Overall, on a year-on-year basis, only Rail Freight and Pipeline transport are still declining. All the other aspects of transport and freight have been in recovery mode, as reflected in the overall increase of 6.4% in the CTFI (based on three-month moving average data and comparing to a year earlier). As the economy gains traction during 2022, a further gradual recovery of the transport sector can be expected.

Graph 3: Changes on a year ago for the Transport and Freight Index and its components (based on a three-month moving average of index values).

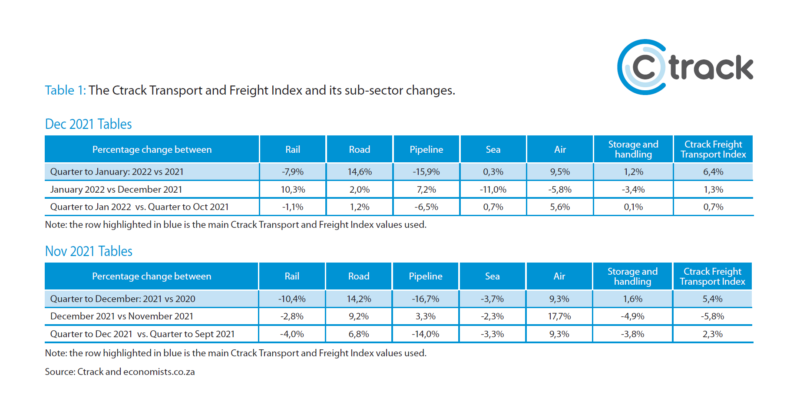

Table 1: The Ctrack Transport and Freight Index changes per period from December 2021 to January 2022 (based on a three-month moving average of index values)